Estimating Linear Intervals

Source:vignettes/Estimating-Linear-Intervals.Rmd

Estimating-Linear-Intervals.RmdWhen using a linear model, we can generate prediction and confidence intervals without much effort. By way of example, we can use workboots to approximate linear model intervals. Let’s start by building a baseline model. In this example, we’ll predict a home’s sale price based on the first floor’s square footage with data from the Ames housing dataset.

library(tidymodels)

# setup our data

data("ames")

ames_mod <- ames %>% select(First_Flr_SF, Sale_Price)

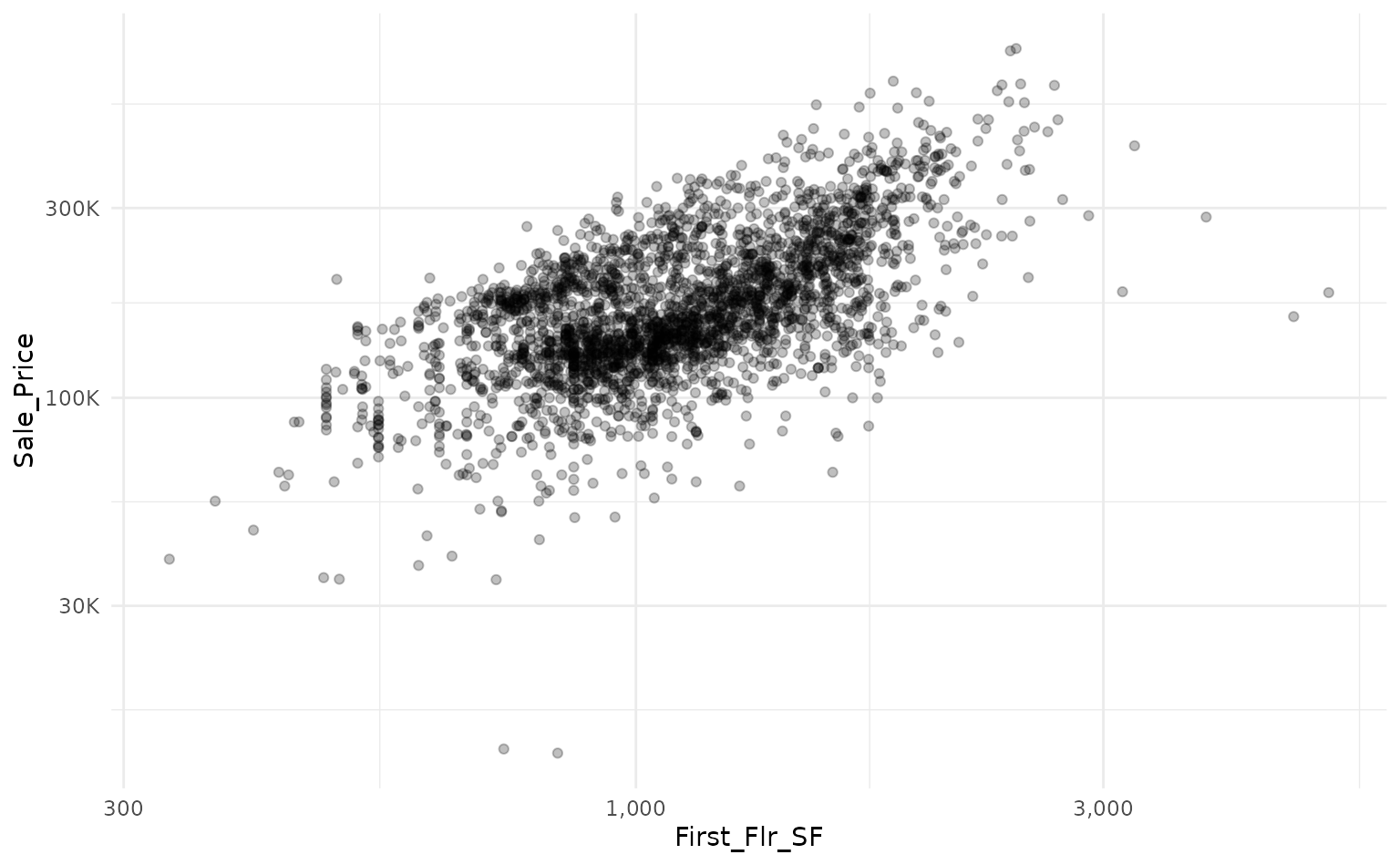

# baseline plot

ames_mod %>%

ggplot(aes(x = First_Flr_SF, y = Sale_Price)) +

geom_point(alpha = 0.25) +

scale_x_log10(labels = scales::comma_format()) +

scale_y_log10(labels = scales::label_number(scale_cut = scales::cut_short_scale()))

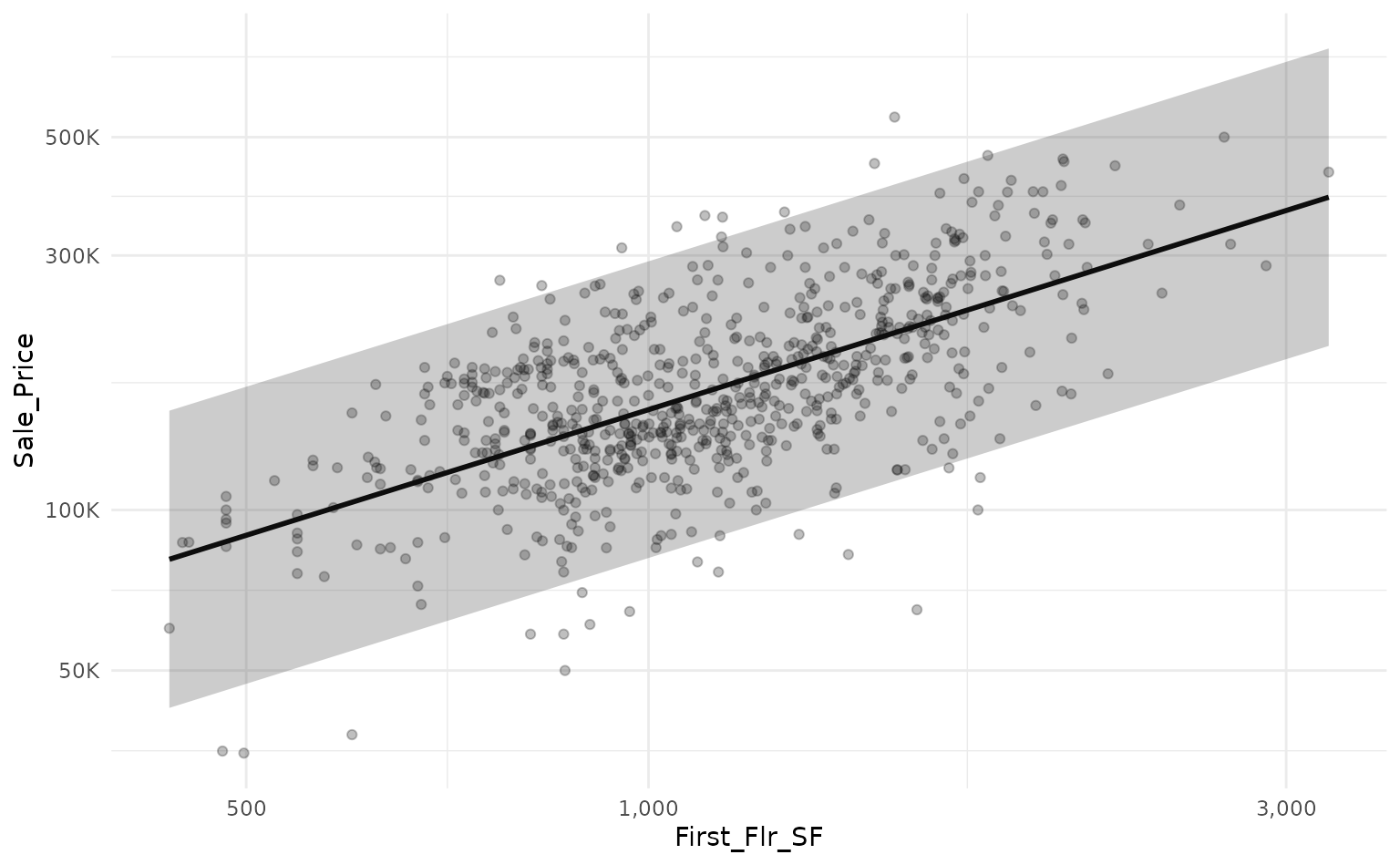

We can use a linear model to predict the log transform of

Sale_Price based on the log transform of

First_Flr_SFand plot our predictions against a holdout set

with a prediction interval.

# log transform

ames_mod <-

ames_mod %>%

mutate(across(everything(), log10))

# split into train/test data

set.seed(918)

ames_split <- initial_split(ames_mod)

ames_train <- training(ames_split)

ames_test <- testing(ames_split)

# train a linear model

set.seed(314)

ames_lm <- lm(Sale_Price ~ First_Flr_SF, data = ames_train)

# predict on new data with a prediction interval

ames_lm_pred_int <-

ames_lm %>%

predict(ames_test, interval = "predict") %>%

as_tibble()

ames_lm_pred_int %>%

# rescale predictions to match the original dataset's scale

bind_cols(ames_test) %>%

mutate(across(everything(), ~10^.x)) %>%

# plot!

ggplot(aes(x = First_Flr_SF)) +

geom_point(aes(y = Sale_Price),

alpha = 0.25) +

geom_line(aes(y = fit),

size = 1) +

geom_ribbon(aes(ymin = lwr,

ymax = upr),

alpha = 0.25) +

scale_x_log10(labels = scales::comma_format()) +

scale_y_log10(labels = scales::label_number(scale_cut = scales::cut_short_scale()))

We can use workboots to approximate the linear model’s prediction

interval by passing a workflow built on a linear model to

predict_boots().

library(workboots)

# setup a workflow with a linear model

ames_wf <-

workflow() %>%

add_recipe(recipe(Sale_Price ~ First_Flr_SF, data = ames_train)) %>%

add_model(linear_reg())

# generate bootstrap predictions on ames test

set.seed(713)

ames_boot_pred_int <-

ames_wf %>%

predict_boots(

n = 2000,

training_data = ames_train,

new_data = ames_test

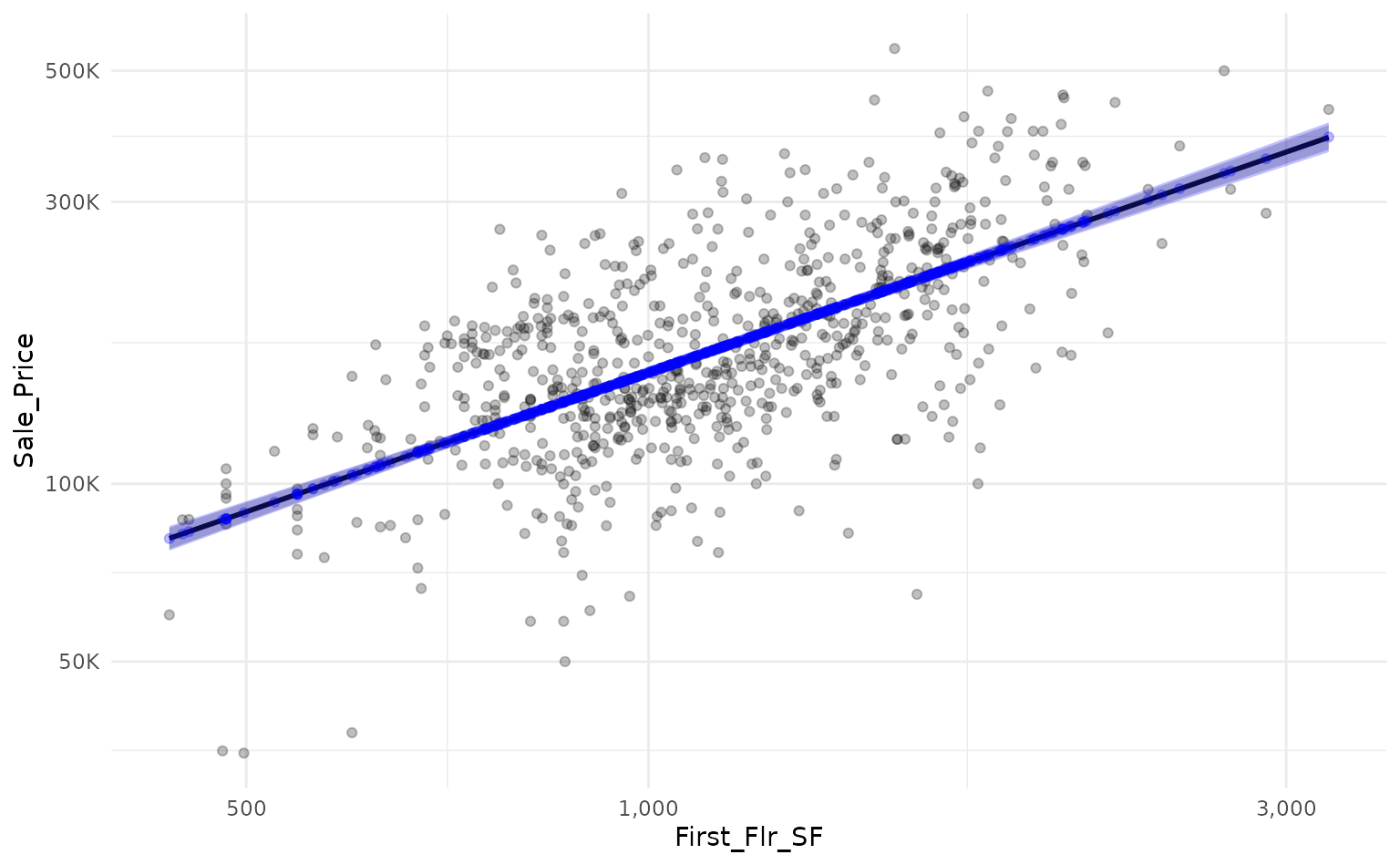

)By overlaying the intervals on top of one another, we can see that

the prediction interval generated by predict_boots() (in

blue) is a good approximation of the theoretical interval from

lm().

ames_boot_pred_int %>%

summarise_predictions() %>%

# rescale predictions to match original dataset's scale

bind_cols(ames_lm_pred_int) %>%

bind_cols(ames_test) %>%

mutate(across(.pred:Sale_Price, ~10^.x)) %>%

# plot!

ggplot(aes(x = First_Flr_SF)) +

geom_point(aes(y = Sale_Price),

alpha = 0.25) +

scale_x_log10(labels = scales::comma_format()) +

scale_y_log10(labels = scales::label_number(scale_cut = scales::cut_short_scale())) +

# add prediction interval created by lm()

geom_line(aes(y = fit),

size = 1) +

geom_ribbon(aes(ymin = lwr,

ymax = upr),

alpha = 0.25) +

# add prediction interval created by workboots

geom_point(aes(y = .pred),

color = "blue",

alpha = 0.25) +

geom_errorbar(aes(ymin = .pred_lower,

ymax = .pred_upper),

color = "blue",

alpha = 0.25,

width = 0.0125)

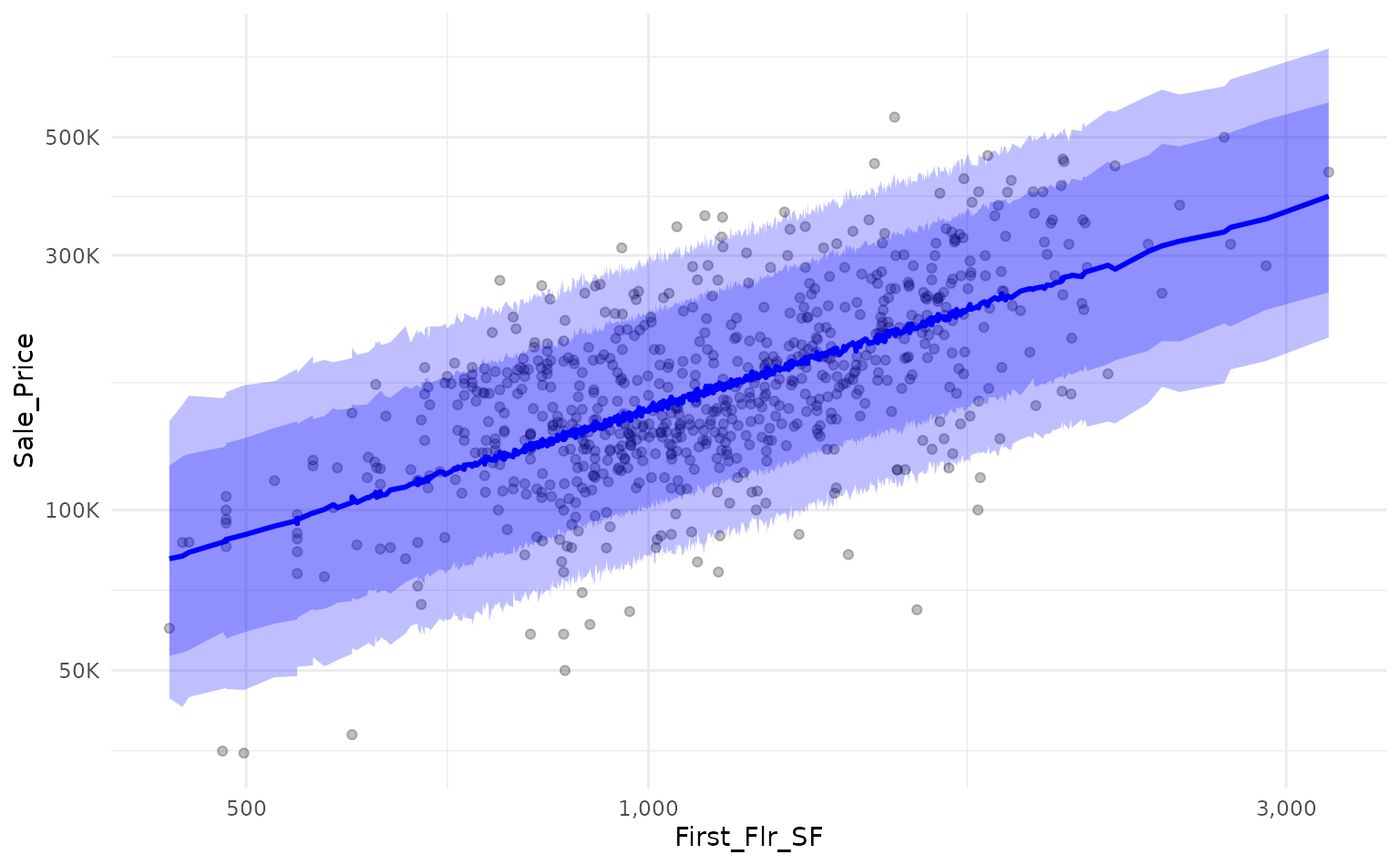

Both lm() and summarise_predictions() use a

95% prediction interval by default but we can generate other intervals

by passing different values to the parameter

interval_width:

ames_boot_pred_int %>%

# generate a 95% prediction interval

summarise_predictions(interval_width = 0.95) %>%

rename(.pred_lower_95 = .pred_lower,

.pred_upper_95 = .pred_upper) %>%

select(-.pred) %>%

# generate 80% prediction interval

summarise_predictions(interval_width = 0.80) %>%

rename(.pred_lower_80 = .pred_lower,

.pred_upper_80 = .pred_upper) %>%

# rescale predictions to match original dataset's scale

bind_cols(ames_test) %>%

mutate(across(.pred_lower_95:Sale_Price, ~10^.x)) %>%

# plot!

ggplot(aes(x = First_Flr_SF)) +

geom_point(aes(y = Sale_Price),

alpha = 0.25) +

geom_line(aes(y = .pred),

size = 1,

color = "blue") +

geom_ribbon(aes(ymin = .pred_lower_95,

ymax = .pred_upper_95),

alpha = 0.25,

fill = "blue") +

geom_ribbon(aes(ymin = .pred_lower_80,

ymax = .pred_upper_80),

alpha = 0.25,

fill = "blue") +

scale_x_log10(labels = scales::comma_format()) +

scale_y_log10(labels = scales::label_number(scale_cut = scales::cut_short_scale()))

Alternatively, we can estimate the confidence interval around each

prediction by passing the argument "confidence" to the

interval parameter of predict_boots().

# generate linear model confidence interval for reference

ames_lm_conf_int <-

ames_lm %>%

predict(ames_test, interval = "confidence") %>%

as_tibble()

# generate bootstrap predictions on test set

set.seed(867)

ames_boot_conf_int <-

ames_wf %>%

predict_boots(

n = 2000,

training_data = ames_train,

new_data = ames_test,

interval = "confidence"

)Again, by overlaying the intervals on the same plot, we can see that

the confidence interval generated by predict_boots() is a

good approximation of the theoretical interval.

ames_boot_conf_int %>%

summarise_predictions() %>%

# rescale predictions to match original dataset's scale

bind_cols(ames_lm_conf_int) %>%

bind_cols(ames_test) %>%

mutate(across(.pred:Sale_Price, ~10^.x)) %>%

# plot!

ggplot(aes(x = First_Flr_SF)) +

geom_point(aes(y = Sale_Price),

alpha = 0.25) +

scale_x_log10(labels = scales::comma_format()) +

scale_y_log10(labels = scales::label_number(scale_cut = scales::cut_short_scale())) +

# add prediction interval created by lm()

geom_line(aes(y = fit),

size = 1) +

geom_ribbon(aes(ymin = lwr,

ymax = upr),

alpha = 0.25) +

# add prediction interval created by workboots

geom_point(aes(y = .pred),

color = "blue",

alpha = 0.25) +

geom_ribbon(aes(ymin = .pred_lower,

ymax = .pred_upper),

fill = "blue",

alpha = 0.25)